Matchmaker or Marketplace: Which is Your Platform?

Over the past few years, the popularity and allure of marketplaces has garnered the attention of consumers, businesses, entrepreneurs, and investors alike. Household brands like Uber, Lyft, Airbnb, and DoorDash have managed to weave their way into the fabric of our daily lives. But for every one unicorn that has managed to prance off into the sunset, there are a handful more stories of marketplaces that have failed. So what gives? What’s the secret sauce for driving successful marketplace platforms?

Before we can answer that question, let’s review the primary objectives of online marketplace platforms. First, they aim to connect buyers and sellers in what would otherwise be a fragmented environment. Second, the platform needs to provide a trusted environment for both parties to interact safely and comfortably. Now, some marketplaces emphasize one objective more than the other, while others can optimize on both. Regardless, the buyers and sellers are always driving toward a common result: a transaction. And that transaction will always involve the delivery of a good or service by the seller and a payment from the buyer.

The key difference lies in what role the marketplace platform plays within that transaction.

The Origins of Digital Marketplaces

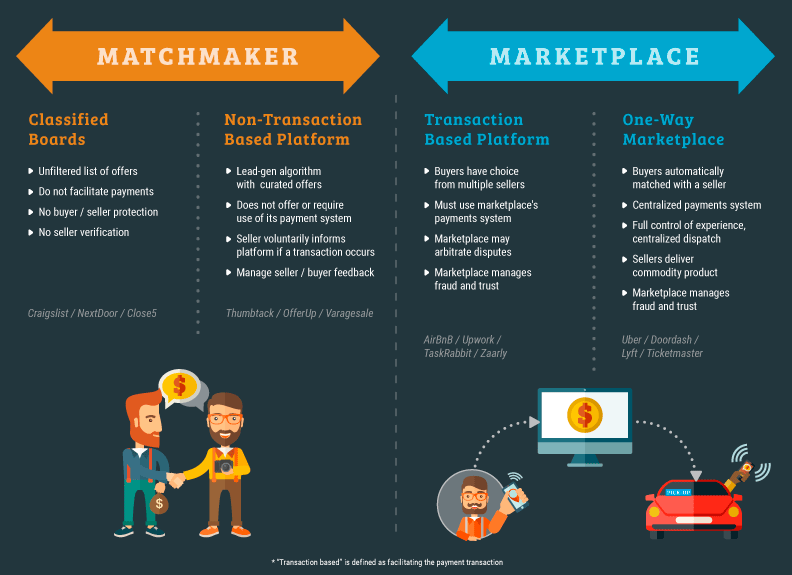

Marketplaces are not a new phenomenon. Both Craigslist and eBay—born long before smartphones and the app economy —are two pioneers of the online marketplace model. Both demonstrated how the Internet made it a) easy for buyers to search and discover products, and b) easy for sellers to peddle their wares to an infinitely larger audience. In other words, both platforms functioned as virtual matchmakers.

While they helped facilitate connections, both Craigslist and eBay stopped short of standing in the middle of the transaction; the payment from the buyer to the seller happened directly. In fact, neither platform even prescribed how a payment should occur. On Craigslist, most transactions still took place using cash as part of a face to face transaction. eBay took it a step further by providing a list of recommendations for sellers to accept payments, but the burden of the actual activity (e.g., setting up a merchant account, dealing with the buyer) lay with the seller. Neither Craigslist nor eBay would collect the payment from the buyer on behalf of the seller. After all, it was the seller who was delivering the good or service, so it made logical sense for them to collect their payment directly from the buyer.

Fast forward 20+ years. Smartphone apps are now the norm and “on-demand” service has become our default expectation. And the marketplace economy that gave us eBay? It’s evolved dramatically. Now, it’s not just physical goods that are being bought and sold, but services that are being sought after and performed by distributed fleets of individuals. With this shift has come a greater emphasis on the role of the marketplace, as a consumer service provider, an income source, and a job creation engine. With Uber, for example, the driver doesn’t just expect to get paid every time she completes a ride, she expects to receive that payment without having to do anything. She doesn’t have to worry about whether her passenger’s credit card is valid. She simply receives the fare. With Airbnb, the marketplace collects payment from the guest and holds it in safekeeping on behalf of the host in order to ensure a smooth exchange and hassle-free transaction. On the freelance marketplace, Upwork, freelancers are assured that they will receive payment for all the hourly work they perform, provided they follow the marketplace’s rules. In all cases, it is the marketplace that is the “merchant of record.” This means that not only does the marketplace receive the buyer’s payment, but they also provide the buyer with customer support if ever a problem or dispute were to occur—this is no longer the responsibility of the individual seller (as was the case with our earlier examples). The end result is a seller/payee that can focus on their work, their brand, their reputation (i.e., feedback rating), rather than on the operational tasks of managing the transaction, all of which is in the best interests of the marketplace.

In today’s environment, marketplaces pride themselves on simple and fluid user experiences. Not surprisingly, the ability to remove any friction around the transaction (both the buyer paying for a good or service, and the distribution of earnings to the seller), is central to their business models. But creating a payment experience that equally satisfies the interests of both buyers and sellers is a tricky balancing act for any marketplace.

Handling Marketplace Transactions

Solutions have cropped up in response to this increasingly important need for marketplaces to seamlessly manage transactions. For example, solutions like Stripe Connect and WePay take steps to remove the pain out of both payment acceptance and payout distribution for platform businesses. On the acceptance end of the payment, they enable every seller within the marketplace to have its own dedicated merchant account. When coupled with a robust suite of APIs, it helps create a friction-free buying experience for consumers, while at the same time giving the marketplace control over the visual look and feel of the payment experience. It enables marketplaces, particularly those at an earlier maturity stage, to focus on their core service offering without being subject to the administrative and operational burden of managing the payment flow. There’s a tradeoff, however, whereby the marketplace is no longer in complete control of the seller’s payment experience. If there’s any problem with the payment—such as a declined credit card charge—there’s little the marketplace can do to intervene and improve the experience. Furthermore, the marketplace isn’t able to control how much gets paid out to the seller because it never touches the payment transaction. For example, a marketplace wouldn’t have the discretion to easily add a bonus to a high-performing seller’s payment because the amount that gets paid is limited to the amount that was charged to the buyer. In order to accomplish this, the marketplace would have to be in complete control of when and how the payout occurred from an independent source of funds, and not solely dependent on the authorization and settlement cycle of the buyer’s credit card transaction.

Matchmakers vs. Marketplace Platforms

Getting back to our original question concerning secret sauces and marketplace success…

At its core, a marketplace ensures a trusted environment for both buyer and seller to transact easily and avoid any anxiety over the payment. Considering the additional value that a marketplace like Uber or Airbnb provides by sitting in the payment value chain, and insulating the buyers and sellers from the awkwardness of exchanging money, it’s incumbent upon nascent marketplace platforms to evaluate their own roles in the transaction. Should they be acting as the “merchant” when it comes to accepting payments from buyers, while independently facilitating the payout to the seller? Or should they connect the buyer and the seller and allow the two parties to transaction directly? There is no right or wrong answer here, but it does demand some introspection among marketplace businesses.

In a true marketplace, the pinnacle of the seller experience is receiving payment, which begs the question: to what degree should the marketplace influence that experience? With the pass-through payment model, each individual seller must deal with payments from multiple buyers with no single intermediary. The burden this creates for the seller can be immense. And yet, in many cases, the pass-through payment solution makes sense, say for a marketplace platform that doesn’t earn a fee on the actual transaction between a buyer and seller, but rather monetizes its business by charging listing fees or lead generation fees. So how does a platform know if they need to stand in the path of the payment flow or let the buyers and sellers transact directly?

The answer is driven by four things:

- The type of service you’re providing.

- How much control the seller user experience on your platform demands.

- The desire to protect the seller from fraudulent buyers.

- Any plans to expand the platform’s geographic and demographic reach to new sellers.

Unfortunately, there are few marketplace transaction solutions that efficiently handle all these criteria at once.

With the Hyperwallet payout platform, we provide the marketplace with complete control over the payment flow, making it easy for the platform to determine how, when, and how much it needs to pay each seller, independent of the payment from the buyer. Hyperwallet also enables the marketplace to easily pay their suppliers and instantly expand their footprint with no infrastructure or local bank account set up required. We partner with marketplace platforms that believe payments are a critical component of the seller experience, and therefore want to retain control over that all-important event in the transaction.